I love quant shops that produce well-reasoned thought pieces with all that “data and stuff” that support well-reasoned and well written pieces generated here at

If one practices “active” investment management, then one implicitly assumes there is some form of inefficiency in financial markets and we can debate its source over cocktails one night. Blackrock…

While all else is never equal, we freeze this debate to make this point. Companies that end up staying in business tend to produce some

From time to time, we get very involved with our investments at the Board level. And one of the points we try to drive through

From the Charles Skorina newsletter: Chief investment officers, investment staffs (and OCIOs) earn serious money for their schools and cost a relative pittance to maintain.

Corpgov.law.harvard.edu is actually a pretty good website that captures most of the bigger governance issues of the day and is a late 2025 signup. This

There has been a lot of ink spilled on the debate entitled: Are Private Fund Sponsors Marking Their Reported NAV to Market or Cost? It

But not the way the fine folks at VerdadCap.com are thinking in another wise, interesting piece. Without the benefit of AI, I read their latest

PE Manager is selling an investment in Fund 1 to its Fund 2 at a discounted value and thus screwing investors in Fund 1.

There is NOT a word for word recitation of the ever expanding mostly made-up laundry list of disclaimers to start an earnings call. Note “there

Having no “plan” makes no sense. Having an “always behind the 8-Ball late, rigid asset allocation that perennially finds new things to do at the

The democratization of private equity is not democracy, it is marketing.

Said another way, watching professional tennis and some other things one might see on screens are really not “models” for activities in which many participate,

If you don’t know who Mark Leonard is, go look at long term stock chart of Constellation Software. And then you might say his opinion

It is good, clean fun to have a day to be right for reasons that didn’t seem to matter the day before. With a nice

The April Proxy statement says 89% of the CEO’s pay is at risk. This is the stock chart. Mr. Trerotola is retiring this year. What

Tricolor, the third-largest used auto retailer in Texas and California, has more than $1 billion in assets and over $1 billion in liabilities, with more

Regulation can be viewed as the Full-Time Employment Act for Lawyers. Some things are complicated both in their nature and the way change can morph

Doomscrolling in financial market journalism and commentary was so “way before” the current cellphone doomscrolling phenomena. And I am sure it was popular on stone

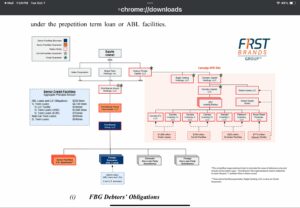

The mind can wander. This is a big corporate bankruptcy, and you haven’t seen many of them, given the sheer tidal wave of dollars that

“Based on analysts’ LinkedIn profiles, we identify a robust negative correlation between the expressive tone conveyed in their self-presentations and forecast accuracy, particularly among male

Process. Interesting. Re-read annually. Deleted half the lists and ideas in the “get to it later” email folder. Reading outside the obvious. Hacking the CSC

Thanks for Re-Tip from the Byrne at the Diff for something I have read periodically since 1983. Translation? The world’s a big place and you cannot

Murray Stahl has been referenced here before. Google away on him and Horizon Kinetics and sit down for some long reads. A great writer he

I lifted this from a recent Financial Times piece. What I will add for the intrepid reader is a longer time horizon. It is correct

This was from a recent Wall Street Journal article. I would simply like to be on an investment committee being pitched “let’s give the kid

revise the definition of “accredited investor” from high-net-worth individuals to anyone who passes a federally mandated exam

If nothing else but by not being REALLY early. And it’s not fair to whomever they are to suggest that the letter lacks little detail