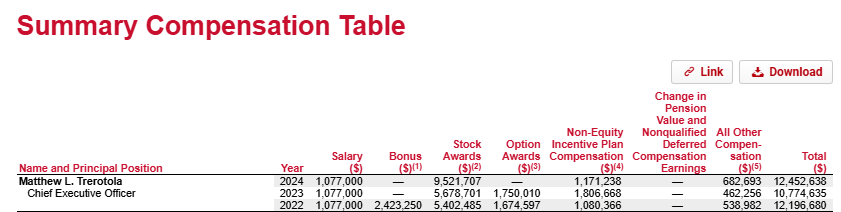

The April Proxy statement says 89% of the CEO’s pay is at risk.

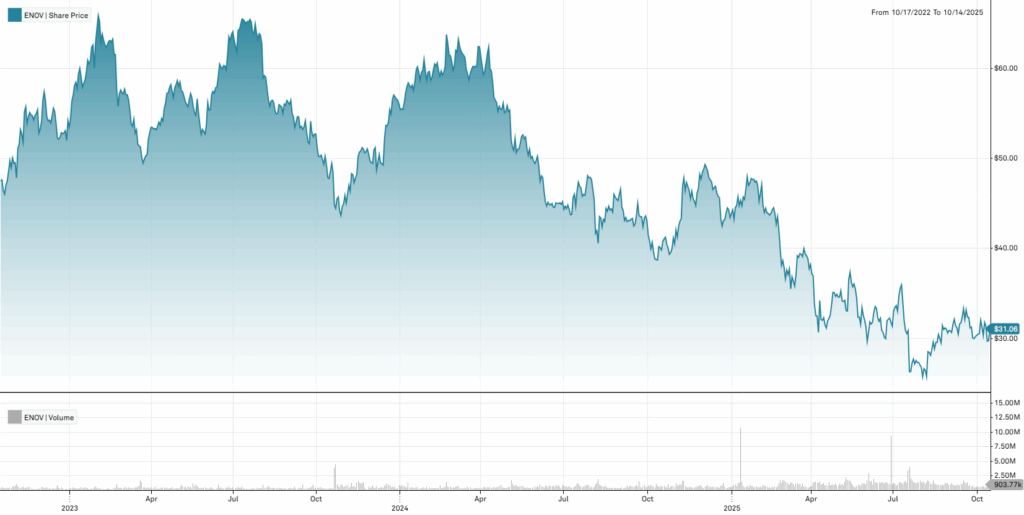

This is the stock chart.

Mr. Trerotola is retiring this year.

What we would say is:

- Trying to acquire your way up an industry food ladder is expensive and unpleasant for shareholders.

- 8 Lines of Adjustments to Earnings should be a giant flag.

- The medical device acquisition and consolidation game is at least ten years OVER.

Note to new CEO: STOP. Show shareholders the money.

And an interesting sidenote. I am not sure why Liam Kelly, the CEO of Teleflex, is on this board because the companies seem to be veering competitively toward each other. But TFX seems to have just run into the same wall.

Both seem cheapish. We own one.