We have written numerous times about the degradation of what constitutes “earnings.” We are talking decades. But excluding compensation issued via stock vs cash is arguably the first issue we wasted thousands of words on. If issuing stock to employees in leu of cash isn’t compensation, then what is it?

Robert Armstrong writes daily in the Financial Times. This is a cull from one of his latest columns. It is a nice re-summary of the issue above. We are tired of the issue. And for reference sake, we don’t own a lot of software and we adjust all earnings with a “just add back 50 percent of SBC and stop talking about it” in our models.

The US software industry is extremely big and important. Just the 10 largest companies have a market capitalisation of $2.9tn — about 7 per cent of the stock market. Microsoft alone accounts for $1.9tn of that.

The way these companies pay their employees and report their results makes them look (to many investors, at least) more profitable than they really are. Many software stocks had a brilliant run between the end of the great financial crisis and the beginning of the pandemic, as investors went all-in for growth. That is changing now, and the industry’s finances may be in for a reassessment. The implications for stock prices are obvious.

The illusion of extraordinary profitability is the fact that software companies pay their employees largely in stock. Many companies report adjusted profits excluding this form of pay. This is insane, for reasons we detailed yesterday.

It is important to understand that this is an industry-wide issue. Mark Moerdler of AllianceBernstein calculates that over the past 10 years, as the good times have rolled, share-based compensation has risen from 4 per cent to almost 12 per cent of revenue for global software companies, on average (median). In an industry with operating margins of 30-40 per cent, that means excluding SBC pumps up operating margins by as much as a third. At younger companies, the figure can be much higher: at Snowflake, a $45bn cloud software company, SBC was 42 per cent of revenue last year — all excluded from adjusted profit.

Established companies are not immune. Adobe has spent $13.5bn repurchasing 31mn of its own shares over the past three years. Over that period, the company share count has fallen by only 21mn shares. Billions in value are leaking out of Adobe every year to pay for something the company (insanely) excludes from adjusted profits.But at companies that do not adjust away SBC, its mere presence makes their results harder to follow. Microsoft is a good example, as we argued yesterday. The point is worth repeating. The company spent $33bn repurchasing 95mn of its own shares last year, but it issued 40mn shares to give to employees. In other words, the company spent something like $13bn of its free cash flow — about a fifth of the cash it generated last year — paying employees.

Anyone who is valuing Microsoft (or other software companies) on cash flow and who doesn’t take the (considerable!) trouble to adjust for SBC is making a mistake. And to the degree that unadjusted cash flow drives software companies’ stock prices, the whole sector may be overvalued relative to other industries.

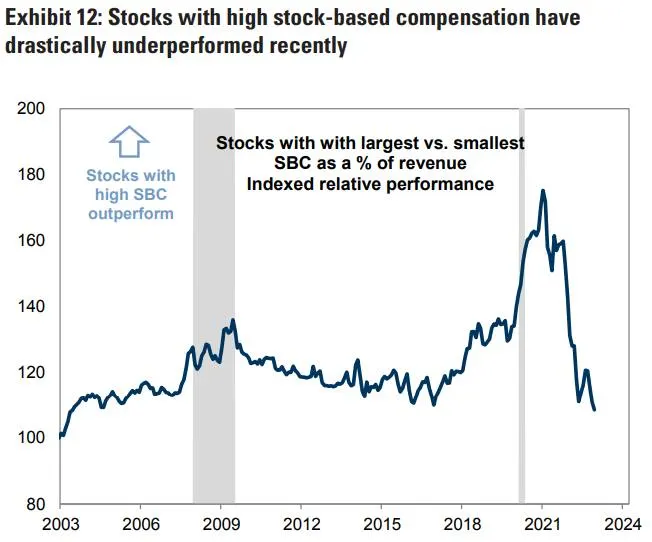

In a note to clients last week, Ryan Hammond’s team at Goldman Sachs wrote that the difference between adjusted and unadjusted earnings is far larger in software than in any other sector. They expects that “the market backdrop will remain challenging for stocks with high SBC and low GAAP margins” as higher rates increase the focus on real profitability. Here is their chart of the relative performance of the top and bottom quartile of the stock market companies, ranked by SBC as a percentage of revenue:

Companies that exclude SBC from adjusted earnings should stop doing so; it’s a shameful practice. And investors should be especially watchful of software companies that buy back a lot of shares. These companies tout buybacks as “returning cash to shareholders”, but a big chunk of the cash often goes to employees instead.