While all else is never equal, we freeze this debate to make this point.

Companies that end up staying in business tend to produce some form of real, touchable cashflow that can either be reinvested back in the business or paid out to its owners in some form. This form used to be termed a “dividend” and the dividend per share divided by the stock price was a dividend yield.

And then somebody’s god invented really good tax lawyers who argued that repurchasing shares instead of paying out cash dividends is an implicit form of cash return which also avoids double-taxation of said cash. And it gives you more flexibility in timing and avoids the third rail of a dividend cut in time of pain. Voila. And thus we have this new analysis which adds up dividend payments + share repurchase to come with with a “total cash return to shareholders” theme and analysis. Neat.

The analysis then runs into the last 20 years problem of egregious issuance of stock based compensation to management teams. To avoid the howls of obvious visual dilution of shareholder value, management commits to share repurchase to keep the shares outstanding constant. So if employees need to be retained, and they are retained through stock issuance vs paying them cash outright, and you are then “forced” to buyback stock for the sole purpose of reducing that dilution, how the heck can all share repurchase be considered a legitimate “return to shareholders” metric? It isn’t and it has to be netted out for the numbers below to make sense and be comparable.

And, as pointed out to me recently by a very smart next door neighbor in our Global HQ in Hermosa Beach, you should really be paying attention to dividend growth rather than current yield. But that is another bedtime story.

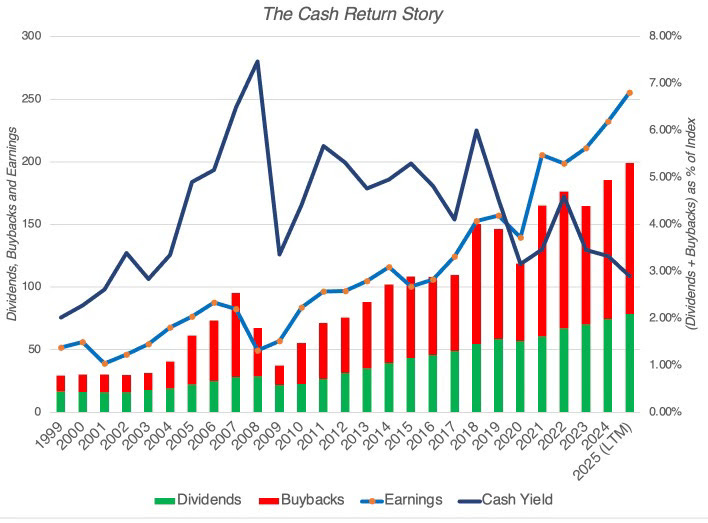

From The Aswath Damodaran Files

2. Healthy cash returns: In conjunction with delivering earnings growth, US companies have also been returning large amounts of cash to their shareholders, albeit more in buybacks than in conventional dividends. In 2025, the companies in the S&P 500 alone returned more than a trillion dollars in cash flows in buybacks, and in the graph below, I look at how the augmented cash yield (composed of dividends and buybacks) has largely sustained the market:

While the dividend payout ratio, computed using only dividends, has been on a downward trend all through this century, adding buyback to dividends and computing a cash yield ratios yields values that are comparable to what dividend yields used to be, before the buyback era.