I love quant shops that produce well-reasoned thought pieces with all that “data and stuff” that support well-reasoned and well written pieces generated here at

It is a long held opinion that supersized voting rights in excess of economic interests is a terrible idea.

If one practices “active” investment management, then one implicitly assumes there is some form of inefficiency in financial markets and we can debate its source over cocktails one night. Blackrock…

While all else is never equal, we freeze this debate to make this point. Companies that end up staying in business tend to produce some

From time to time, we get very involved with our investments at the Board level. And one of the points we try to drive through

From the Charles Skorina newsletter: Chief investment officers, investment staffs (and OCIOs) earn serious money for their schools and cost a relative pittance to maintain.

The concept of holding yourself out to the world as someone still willing to selectively accept “other people’s money” in a professional money management capacity

Corpgov.law.harvard.edu is actually a pretty good website that captures most of the bigger governance issues of the day and is a late 2025 signup. This

PE Manager is selling an investment in Fund 1 to its Fund 2 at a discounted value and thus screwing investors in Fund 1.

There is NOT a word for word recitation of the ever expanding mostly made-up laundry list of disclaimers to start an earnings call. Note “there

The democratization of private equity is not democracy, it is marketing.

The recent fun and games involving the NBA and the gambling indictments are certainly amusing on their own merits, but do they say something

Regulation can be viewed as the Full-Time Employment Act for Lawyers. Some things are complicated both in their nature and the way change can morph

Doomscrolling in financial market journalism and commentary was so “way before” the current cellphone doomscrolling phenomena. And I am sure it was popular on stone

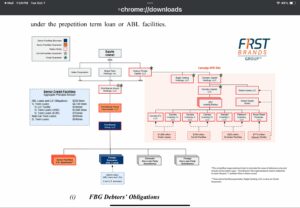

The mind can wander. This is a big corporate bankruptcy, and you haven’t seen many of them, given the sheer tidal wave of dollars that

“Based on analysts’ LinkedIn profiles, we identify a robust negative correlation between the expressive tone conveyed in their self-presentations and forecast accuracy, particularly among male

Process. Interesting. Re-read annually. Deleted half the lists and ideas in the “get to it later” email folder. Reading outside the obvious. Hacking the CSC

Thanks for Re-Tip from the Byrne at the Diff for something I have read periodically since 1983. Translation? The world’s a big place and you cannot

This was from a recent Wall Street Journal article. I would simply like to be on an investment committee being pitched “let’s give the kid

revise the definition of “accredited investor” from high-net-worth individuals to anyone who passes a federally mandated exam

“It is difficult to get a man to understand something when his salary depends on his not understanding it.” The former wrote the attached piece,

Charlie Munger, the former vice chairman at Berkshire Hathaway, has a take on drawdowns worth quoting in detail: “I think it’s in the nature of long-term

Rarely has a man been so quoted and so rarely followed, except maybe Christ and Mohammed. “Dude, I was at Berkshire with my buddies…are you

Despite the usual breathless fawning, let’s face it, Buffett’s latest letter reads as if it’s the last one and he duly notes it. And it’s

Charles Skorina is an interesting “old hand” – CharlesSkorina.com – who runs an executive search firm for the endowment world. And I like his letter.

A few hundred years ago, shortly after beginning Phase II of life as Cove Street Capital, I was “summoned” to a very large allocator organization, after 10 years of annual treks and pitches to zero avail.

I like writing about investing. I wrote a quarterly investment letter for the fund when semi-annual was all that was required. But the nonsense that